Australian authorities items US$190 million to Telstra to purchase Digicel

On 25 October final yr, Telstra and the Australian authorities agreed to pay US$1.6 billion (A$2.1 billion) for Digicel Pacific. The acquisition was broadly reported on the time, however there was little evaluation of the phrases and situations since. Utilizing publicly out there data, we present that the Australian authorities has signed off on a high-return, low-risk deal for Telstra.

As Digicel is a privately held firm and monetary details about it’s restricted, our evaluation is predicated totally on Digicel’s 2020 debt-restructuring submitting to the US Securities and Change Fee, and Telstra’s media briefing on the acquisition. Our intention is to calculate the deal’s inside price of return (IRR) – a key measure of the anticipated profitability of any mission – for each the Australian authorities and Telstra.

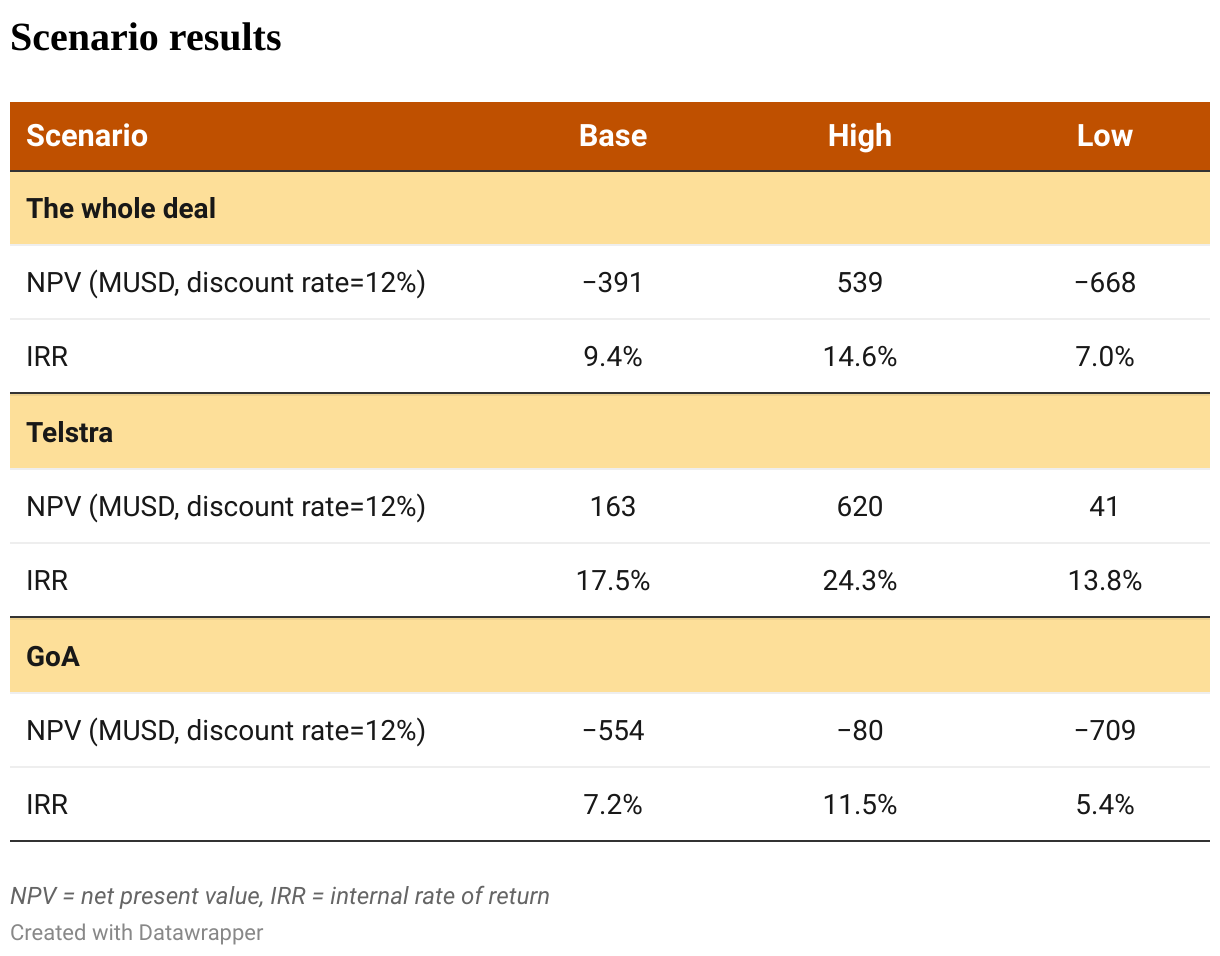

Primarily based on the perfect assumptions we might make based mostly on data within the public area (see the notes on the finish of this put up, and the accompanying spreadsheet), our mannequin estimates an IRR of 9.4% for the deal as an entire, which might be described as modest. However how do every of the 2 events (Telstra and the Australian authorities) fare? Telstra itself will solely contribute US$270 million of the $1.6 billion complete, with the Australian authorities funding the remaining $1.33 billion (all figures in US$).

Telstra executives made it clear at its press convention that, below the settlement with the Australian authorities, it’s entitled to obtain dividends of $45 million instead of all funds to the Australian authorities for the primary six years (that’s, till it has its funding again). Telstra executives additionally stated that the Australian authorities will lend it $720 million at a “aggressive” rate of interest “modestly under Telstra’s blended price of debt”. Telstra’s press convention remarks point out that $360 million will likely be given at a hard and fast return (with a “coupon price” that Telstra says is “a stage of a bit above our present price of debt”). The ultimate $250 million is subordinated fairness.

With these assumptions, we estimate that the IRR for Telstra is 17.5% and for the Australian authorities 7.2%. A 17.5% IRR is spectacular. Assuming a weighted common price of capital of 12%, it’s equal to the Australian authorities gifting $190 million to Telstra, which is 70% of the $270 million Telstra is definitely paying.

This excessive anticipated return is nearly assured, as Telstra is taking nearly not one of the threat. Among the many protections being supplied by the Australian authorities are: nearly full safety of Telstra’s money stream within the first six years; partial safety after that by the supply of fixed-return fairness; provision of political threat insurance coverage; and safety all through by way of assumption of all of the overseas trade threat. The difficulties of repatriating dividends from PNG operations are well-known. That job of changing kina to Australian {dollars} will fall to the Australian authorities slightly than Telstra.

We additionally ran a state of affairs evaluation with high and low instances. Within the excessive case (after factoring within the extra funds which have been agreed on this state of affairs), Telstra’s IRR is 24%; within the low case it’s 14%. In different phrases, even the draw back is engaging, and the upside is mouth-wateringly so.

Regardless of strolling away with such a high-return, low-risk deal, Telstra is below no obligation from the Australian authorities to increase PNG’s cell phone sector, or to supply higher companies, or to scale back costs. Having been threatened by the PNG authorities with a monopoly tax, Telstra has not too long ago undertaken to increase Digicel’s community of towers, but it surely might be that this additional will increase its earnings. The true check will likely be whether or not Telstra is ready to scale back costs, as Digicel has persistently failed to do lately.

The Australian authorities subsidy to Telstra offers a brand new benchmark within the retreat of financial rules from the coverage area, and their alternative by unspecified safety issues. For this company welfare deal to undergo, it was enough that Telstra is Australian not Chinese language.

Notes:

Restricted historic information is obtainable on income development. We assume income development of three% from FY22-23 to FY34-35, equal to the income development price in FY18-19 in PNG, Digicel Pacific’s greatest market. We additionally assume that the EBITDA (income minus prices apart from tax, curiosity, depreciation and amortisation) can be 56% of income. That is above the three-year common from FY18-19 to FY20-21 of fifty%, because the PNG authorities has estimated greater earnings for Digicel below Telstra possession resulting from an finish of licensing (revenue shifting). Working again from the estimated enhance in tax ($11 million; all figures in US$), this means a rise within the EBITDA ratio from 50% to 56% within the base FY22-23 yr. Digicel studies on an April-March monetary yr, however we comply with the Telstra July-June monetary yr, assuming that the acquisition of Digicel happens in FY21-22 and that the primary yr of operation of Digicel by Telstra is FY22-23.

Capex to gross sales is assumed at 15%, as per the media briefing. Depreciation and amortisation (D&A) to capex is assumed at 1.25, as per the Digicel Group’s ratio in FY18-19, and in step with Telstra’s touch upon the topic that Digicel Pacific has “structurally decrease capex than D&A”. The terminal web money stream price is 0.5% from FY35-36 onwards.

Liabilities include a pre-existing $95 million Digicel PNG facility for the interval from FY19-20 to FY24-25, and the $720 million mortgage from the Australian authorities. Telstra executives stated that the rate of interest on the latter will likely be “modestly under Telstra’s blended price of debt”. Since Telstra’s common price of debt is 3.8%, we assume the price of this authorities debt to be 3.5%. $360 million from the Australian authorities (GoA) will likely be given at a hard and fast return (with a “coupon price” that Telstra says is “a stage of a bit above our present price of debt”). We assume 5%. When it comes to seniority, it’s assumed that Telstra should get its assured $45 million per yr; then the GoA mortgage is paid again, then the GoA coupon-paying fairness, after which the GoA subordinated fairness (assumed to get the identical return because the Telstra fairness after the primary six years). All earnings are returned as dividends, and PNG applies a company tax of 30% and a withholding tax of 15%. The IRRs are earlier than tax in Australia.

Within the excessive case, income (terminal money stream) development is 10% (1%), and within the low case 0% (0%), in comparison with the bottom case’s 3% (0.5%). Within the excessive case, the set off for $250 million in extra (earn-out) funds to Digicel is activated. We assume $50 million of that is fairness from Digicel and $200 million from Australia, based mostly on the announcement that the earn-out fee will likely be shared between the Australian authorities and Telstra on an 80/20 foundation. We assume that these extra funds are within the type of fairness and don’t have an effect on the distribution of dividends.

Knowledge and calculations used on this weblog can be found on this Excel spreadsheet.

Neither the Australian authorities nor Telstra responded to requests for feedback.

Comments (0)